{kind=link}

10 Best Data Leak Detection Tools Today

What is Data Leak Detection Software? Data Leak Detection Software is a specialized security solution that helps …

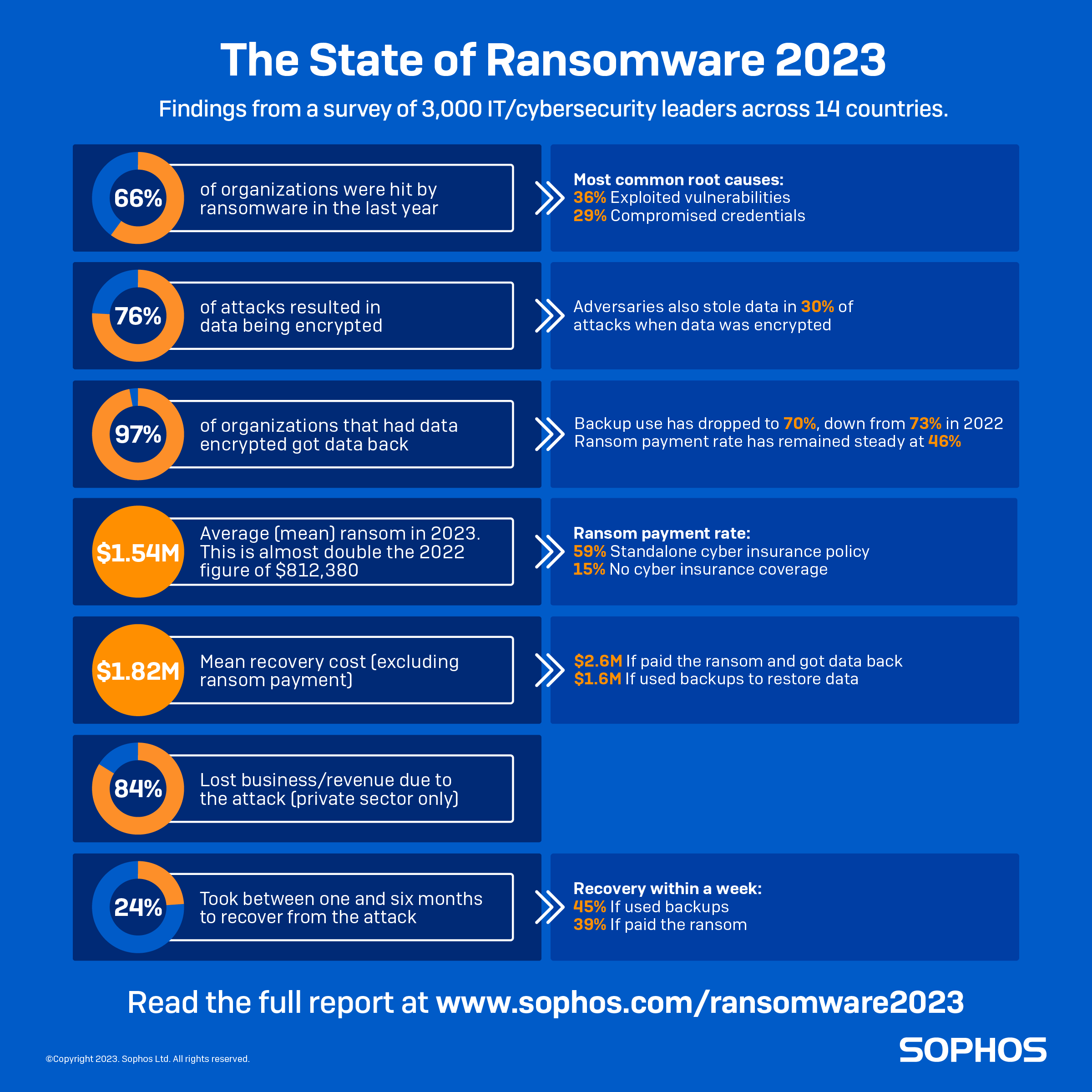

Fact: The average ransomware payment made last year was USD 1.54 million, which is almost double the amount from the previous year.

Add to that another USD 1.82 million (excluding the actual ransom payment) to recover from the attack.

Cyber attacks are expensive and without the proper resource in place many businesses could not weather the storm.

In this post we’ll cover what cyber insurance is, why businesses need it, the types of data that attackers target and how to use insurance to recover from the breach.

Just to make sure we’re on the same page, cyber insurance is also known as cyber liability insurance or cyber risk insurance, so when we talk about cyber insurance, these all mean the same thing.

Cyber insurance is a type of insurance policy designed to help businesses mitigate the financial risks associated with cyber threats and data breaches.

It provides coverage for expenses that arise from a variety of cyber incidents, including data breaches, cyberattacks, ransomware, hacking, and other forms of cybercrime.

Cyber insurance policies typically cover costs related to:

Traditional insurance policies, like property or general liability insurance, often have limited or no coverage for cyber-related risks. Cyber insurance was created specifically to cover these risks.

The frequency and sophistication of “cyberattacks” are continuously increasing. Businesses of all sizes are targets for data breaches, ransomware, phishing, and other cyber threats. Couple that with the costs associated with getting hacked which are substantial. According to the latest IBM Cost of a Data Breach Report, the average cost of a data breach reached an all-time high of USD 4.45 million. This number includes expenses for forensic investigations, legal fees, notification costs, credit monitoring services, fines and settlements.

In the aftermath of a breach, businesses often need to deal with lawsuits from customers, partners, or other third parties affected by the breach. In addition to these legal issues, depending on the industry there may fines involved due to a lack of compliance with various regulations that can get quite expensive.

Beyond the initial remediation costs, cyberattacks often disrupt normal business operations, leading to downtime and loss of income. Even once the business is back up and running there’s reputational damage from the loss of customer trust and negative publicity.

Cyber insurance provides financial protection and can help support the business during an incident as well afterwards. The insurance policy can help cover the cost of forensic investigations, legal fees, notification costs, credit monitoring services, and potential fines or settlements.

Attackers target various types of sensitive data. Some of the most common types include:

Unauthorized access to any of these types of data can have significant legal, financial, and reputational consequences for businesses. This is why having the proper defenses in place, a data breach response plan and cyber insurance is critical as part of a comprehensive risk management strategy.

Cyber insurance plays an important role in the recovery process from a data breach, providing financial support and resources. Recovering from a data breach requires a coordinated effort, involving the organization’s technical, legal, and PR teams.

The first step is containment. Isolate all affected systems to prevent further spread of the breach. Engage your incident response team and any external experts as needed to analyze the breach and determine its scope and impact.

Next you need to removed the threat from you systems. If possible, restore affected systems from backups after you can ensure they are clean and secure. Apply any missing patches and upgrade your security defenses to prevent similar attacks. Always preserve evidence for future investigations and legal purposes.

Depending on the type of data leaked, you may be required to notify relevant authorities and stakeholders. This may be law enforcement, regulatory bodies, as well as affected individuals. Always communicate transparently with your customers, employees, and partners about the breach. Describe the breach’s impact and the steps being taken to address it.

Once you’re able to resume normal operations, ensure that you have the proper security measures and monitoring tools to detect and prevent future breaches. Based on the evidence you saved previously, conduct a post-incident review to identify the root causes of the breach as well as lessons learned. Update your incident response plan, security policies, and employee training programs based on the findings.

RECOMMENDED READING: What a Company Should Do After a Data Breach

While preventing a data breach in the first place is obviously ideal, life happens and a data breach insurance policy can help cover the costs associated with a cyber attack. If you do experience an attack, use it as an opportunity to improve your processes, policies and response plans. Having cyber insurance can provide you with the resources to weather the storm and come out stronger on the other end.

What is Data Leak Detection Software? Data Leak Detection Software is a specialized security solution that helps …

What types of data get breached or leaked Chances are, if you’re reading this, you want to search for your company’s …